This guide contains valuable information, tips, and answers to frequently asked questions, and is geared toward anyone looking to buy a home along the Emerald Coast in Florida. Whether you’re a first-time home buyer or a tenth-time home buyer, you’ll find the details you need.

The Home Buying Process

Set your budget and get pre-approved for a mortgage

Find your ideal home through online listings and view with your real estate agent

Make an offer and secure a contract

Complete due diligence with a home inspection, documents review, and appraisal

Close the deal, pay closing costs, and move into your new home

Set your budget and get pre-approved for a mortgage

Find your ideal home through online listings and view with your real estate agent

Make an offer and secure a contract

Complete due diligence with a home inspection.

documents review, and appraisal

Close the deal, pay closing costs, and move into your new home

Before Shopping for Home – a Checklist

Before Shopping for Home – a Checklist

Do you have earnest money ready?

You’ll need to have between .5% – 2% of the purchase price of a property available within 3 days to put down as earnest money when you submit a contract. More on earnest money deposits on a coming page

Do you have inspection money ready?

You’ll need $250-$1000 for inspections once your offer has been accepted. Pools, pests, and wells can add to this cost.

Do you have a pre-approval?

Writing an offer without a pre-approval letter will put you at a disadvantage in the market.

Do you have a back-up plan?

Things won’t always go according to plan – for example, your lease may expire before your new home closes! Always have a backup plan.

Are you ready for this process?

Buying a home is exciting, but it does require some work! Be prepared for all of the documentation and learning you’ll be doing along the way.

Where to look for homes

Most home buyers will start “shopping” on Zillow, Redfin, etc.

Unfortunately, a lot of these sites can have inaccurate or outdated information. The best place to look is via the MLS, which you can search via access provided by a REALTOR®, or through their website (which is connected to the MLS and updates every 15 minutes).

Make sure to also look at homes that have recently sold in your price range. This will help set expectations about what will likely be available for you in your desired price range and area.

Buyer Brokerage Agreements

Your REALTOR® will ask you to sign something called a Buyer Brokerage Agreement. Essentially, this is a contract which describes the working relationship between you and your Agent, and the responsibilities of each party.

Working with an agent is just like working with any other type of professional – there are guidelines for working together, and this document helps make sure everything is clear to both parties.

Get Pre-approved

What is a pre-approval?

Realty ONE Group requests that all our buyer customers provide proof of cash funds or a pre-approval letter prior to submitting an offer on a property. Buyers can obtain a pre approval letter by applying through a lender and providing the required paperwork. The lender will indicate what loan amount you are pre-approved for, and will also provide estimates on fees, costs associated with the loan, and monthly payments.

*Note: a pre-qualification and a pre-approval are not the same! Always try to obtain a pre-approval as it’s more in-depth and provides a firmer estimate.

What NOT to do after getting pre-approved

The loan approval process can be tricky, so save yourself some heartache by avoiding some of these complications:

Do not make any major purchases (boat, jewelry, motorcycle, furniture, etc.) until after close.

Do not apply for any new lines of credit.

Do not pay off any charges or collections unless directed by your loan officer to do so.

Do not make unusual deposits or move money around from one bank account to another.

Do not change jobs.

There is more to the story

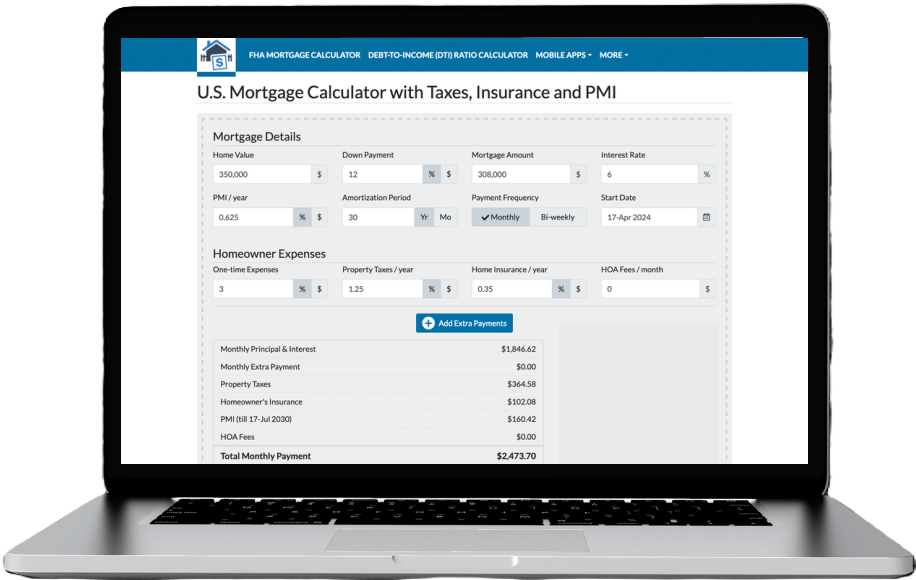

Your pre-approval letter says $500k, but what does that really mean?

That amount is actually broken down into a monthly payment that the lender qualifies you for, based on the following breakdown:

Property Value: $500,000 Down Payment: $100,000 or 20% Principal: $400,000 Interest: 6% Annual Tax: $2,500 Annual Insurance: $2,500 HOA (Monthly): $500 Total Payment: $3314.87

Your pre-approval at $500k really means you’re qualified for a home with a monthly payment of $3315. Keep an eye on HOA , taxes, or insurance costs which could put you over your allotted monthly amount.

Used for a primary residence, second home, or rental property.

Typically for a primary residence

Available to military service members and their families for a primary residence

Available for certain properties for a primary residence

Conventional

Used for a primary residence, second home, or rental property.

Fixed rates, Adjustable rates (ARMs) and terms from 10 to 30 years

Down payments as low as 3% (typically 5%)

No monthly mortgage insurance with a down payment of at least 20%

Mortgage insurance is cancelable when home equity reaches 20%

Fixed rates, Adjustable rates (ARMs) and terms from 10 to 30 years

Fixed rates, Adjustable rates (ARMs) and terms from 10 to 30 years

Typically a great interest rate, terms from 15 to 30 years

Fixed rates and terms for 30 years only.

FHA

Typically for a primary residence

Fixed rates, Adjustable rates (ARMs) and terms from 10 to 30 years

Down payments as little as 3.5%

Mortgage insurance stays for the life of the loan (unless refinanced)

Loan requirements are not as strict as conventional

Down payments as low as 3% (typically 5%)

Down payments as little as 3.5%

Can finance a home up to 100%- no down payment required

Can finance a home up to 100% – no down payment required

VA

Available to military service members and their families for a primary residence

Typically a great interest rate, terms from 15 to 30 years

Can finance a home up to 100%- no down payment required

No mortgage insurance!

VA Loan limits may apply

No monthly mortgage insurance with a down payment of at least 20%

Mortgage insurance stays for the life of the loan (unless refinanced)

No mortgage insurance!

No mortgage insurance!

USDA

Available for certain properties for a primary residence

Fixed rates and terms for 30 years only.

Can finance a home up to 100% – no down payment required

No mortgage insurance!

No acreage limitations

Mortgage insurance is cancelable when home equity reaches 20%

Loan requirements are not as strict as conventional

VA Loan limits may apply

No acreage limitations

What should I look for when comparing loans?

Is the rate locked? Did you want it to be?

Is the loan amount what you were expecting?

Is the rate fixed or adjustable?

Are there discount points included? Did you want them?

Is the loan type what you expected?

Does the loan have a prepayment penalty?

Is the estimated total monthly payment acceptable?

How do origination charges compare to other lenders?

Is the homeowner’s insurance premium accurate?

Are the estimated property taxes accurate?

Is the estimated cash to close as expected, and do you have enough?

Is there an expiration date for the loan estimate?

Sample Loan Estimate

Sample Loan Estimate

Yay! We found the home we want!

Now what?

Writing an Offer

You’ll want to start by asking your agent to submit an offer. Your agent should have already done a buyer consultation with you, which will provide them with some of the information necessary to tailor the offer to your needs. Each offer is unique though, so there will be some details to iron out, such as:

Purchase Price

Earnest Money Deposit (more on this in a bit)

Inspection period and seller contribution to repairs

Type of contract (As-Is vs. Standard)

Financing needs

Closing timeline

And possibly more…

The following slide includes a video walk-through of the FAR/BAR As-Is contract. It is essential that you watch this video and understand all aspects of that document!

The Back-Up Plan!

If you see a home you love and it’s already under contract,

try to write a back-up offer. You never know when a contract will fall through!

You can still shop while you have a back-up offer pending. You just need to pull that offer back if you find another home you love.

Know your purchase contract!

By the time you’re ready to write an offer, you should have already familiarized yourself with the contract of choice for your REALTOR®.

At the end of this document, you will find a walkthrough of the Florida Association of REALTORS As-Is Contract. You are strongly encouraged to read through these pages so you have a preliminary understanding which can support a more in depth contract discussion with your agent.

*The information provided on this document does not, and is not intended to, constitute legal advice; instead, all information, content, and materials available on this document are for general informational purposes only. Information on this document may not constitute the most up-to-date legal or other information. This document contains links to third-party websites. Such links are only for the convenience of the reader, user or browser. Readers of this document should contact their attorney to obtain advice with respect to any particular legal matter.

What can I do to make my offer

more attractive?

In general, less is more - the less you ask of a seller, the more likely you are to get your offer accepted

Lower the amount requested for seller contribution to repairs

Buyer pays for title (in some counties this is common anyway)

Buyer pays for home warranty

Shorten the inspection deadline period

Increase the earnest money amount

Shorten the earnest money deposit period (provide along with the offer or within 1 day)

How Does the Earnest Money

Deposit Work?

An earnest money deposit, or EMD, is money deposited alongside (or quickly following) a purchase contract offer. It is a way for the buyer to indicate to the seller that they are committed to the success of the transaction.

An EMD is held by an escrow or title company, and often applied to the final cost of the home purchase. However, the EMD is also retainable by the seller in case of buyer default on the contract. The sample contract provided with this document contains specific details on how and when a buyer defaults, and how that affects the EMD.

The amount of earnest money paid depends on the market and the condition of the house. In most markets, the average deposit is between .5% – 2% of the property. A higher amount can encourage the seller to take your offer over another competing offer. Your agent can help you decide on the appropriate deposit for your situation.

Congratulations! Your offer was accepted!

While getting an offer accepted is something to celebrate, the work isn’t over yet! Be prepared for quite a bit of items to get through before the home is yours. Common contingencies to expect:

• Home inspection

◦ Most inspections come back with something on them – it doesn’t mean the deal is over, but be prepared for additional negotiation with the seller in some circumstances.

◦ Speciality inspections may also be required (pest, pool, septic, solar, etc.).

• Appraisal

◦ The house must appraise to the right value for the lender to provide funds – if not, renegotiation of the sale price or paying the difference may be required.

• Financing Approval

◦ Lots of documentation will be required from your lender! You’ll need to respond to the lender in a timely manner as you must obtain financing within the required timeline.

But wait, there’s more...

There is one additional item a buyer will be responsible for obtaining between the time of an accepted offer and signing documents at the closing table: insurance. Depending on the property, this can include:

• Homeowner’s insurance

• Speciality insurance such as flood or hurricane insurance

◦ Best practice is to apply for insurance the moment you sign a sales contract so you don’t delay closing. Additionally, be aware if insurance premiums put you over your total monthly payment budget or allowance from the lender.

I will connect you to our partner, Defender Insurance, early on so we have no delays!

What to Expect With Fees and Closing Costs

There are several fees that you will encounter in the home-buying process.

The most accurate information is available from both your lender and the title company (both of which will be charging fees). Historically, buyers’ closing costs have been around 3-4% of the purchase price of the property.

Brokerage Representation Agreement costs are negotiable and, much like the other closing costs, not financeable.

What is Title Insurance and Why Do I Need It?

Title insurance is a type of coverage for you as the new homeowner. Imagine that after moving into your new home, someone claims that your sale was fraudulent and they are the rightful owner. Title insurance protects the policyholder (either the lender or the buyer) from losses resulting in ‘defects’ in the title (meaning issues with the chain of ownership).

A lender’s title policy insures the validity and enforceability of the mortgage – making it possible for the lender to resell the mortgage if they choose.

An owner’s title policy protects the buyer’s ownership right to the home.

How Do Agents Get Paid?

No one works for free, right? There are a few ways that real estate agents can get paid:

Seller offers compensation to be paid to both the listing and buyer agents

Buyer pays the buyer agent and Seller pays the listing agent as one of their closing costs*

Seller pays some of the buyer agent commission and the buyer makes up the difference

*Note: VA buyers are not allowed to pay buyer agent fees, so those will have to be covered by the Seller.

Buyer’s Responsibilities

Get loan pre-approved before looking at homes

Define what you’re realistically looking for

Understand what the contract states before signing

Deposit earnest money within the deadline

Set up and attend inspection walk-throughs

Set up home insurance to lender requirements

Attend closing, on time, with the appropriate identification, and the necessary funds to close.

Be honest, upfront, and communicative through the entire process

Agent’s Responsibilities

Inform and guide you through the process

Set up an MLS search

Schedule all showings within a timely manner

Write and negotiate all offers on the buyer’s behalf

Coordinate with the lender to get necessary documents as requested

Advise the buyer to the best of my ability but leave the decision to them

Respond to messages in a timely manner within my business hours

Coordinate walk-through and closing times

Be honest, authentic, and trustworthy throughout the entire process

Frequently Asked Questions

Does the seller have to respond by the offer acceptance deadline?

No, they do not. They can simply stay silent on the offer if they choose.

Can I put in multiple offers?

Only if you can afford all homes if the offers were accepted. If not, then you must stagger offers (for example, put an expiration date on the first offer and start the new one when the first one expires).

After seeing a home I like, when should I submit an offer?

ASAP. Buyers have lost homes because they couldn’t decide to make an offer fast enough.

Frequently Asked Questions

What do HOAs typically cover?

An HOA can cover a lot or a little. It’s best to request and read through the association guidelines.

What is the appraisal?

An appraisal is an unbiased estimate of the true or fair market value of a home. Lenders require appraisals during the mortgage process so there is an objective way to measure the home’s value and ensure the mortgage amount is appropriate.

What happens if the home appraises below the offer price?

There are a few options, but the process cannot continue without addressing the difference. The seller can choose to drop the price, the buyer can pay the difference out of pocket, or the buyer and seller can agree to compromise (e.g. the buyer pays half the difference out of pocket, and the seller drops the price by the other half).

Frequently Asked Questions

What if I change my mind about the house?

Legally you must cancel for one of the reasons allowed for in the contract, by the appropriate deadline. In a scenario where you are canceling the contract for a reason outside of the allowed situations, the seller has the right to pursue legal action including going to court.

What happens if we find an issue during inspection?

Depending on the contract, the seller may or may not be required to repair the issues found on inspection. Repairs could also be limited to a certain dollar amount, per the contract. If you are using an as-is contract, you are able to cancel the contract for any reason during the inspection period, and the seller is not required to make repairs.

Frequently Asked Questions

What is escrow?

Escrow is where a neutral third party, known as the escrow agent, holds money or assets on behalf of the two parties in the transaction. In real estate, this usually involves the holding of earnest money deposits.

Do I get my deposit back if I cancel the contract?

Only if you cancel for one of the contractually allowed reasons, within the appropriate timelines. Otherwise, the seller may be entitled to retain the deposit.

Frequently Asked Questions

What if the seller’s repair limits allows only some of the repairs?

In the standard contract, the buyer has the right to cancel due to inspection-related issues as long as you are within the inspection period, and as long as the contract does not allow the seller to make the necessary repairs within the stated monetary limits. In an as-is contract, the buyer can cancel for any reason during the inspection period.

What are concessions and how do they work?

Concessions are credits the seller pays to the buyer to cover closing costs. Concessions can only be used to cover the cost of closing, not to put towards the down payment or home improvements.

Frequently Asked Questions

What if I can‘t be there on day of closing?

If you’re not in the local area on the day of closing, we can arrange a remote closing for you – some companies allow online notary and others require the notary be in person with you. It’s a simple process but we need a little lead time to make the arrangements.

What if parties on the contract won‘t be together day of closing?

In this situation, we need a power of attorney executed for one person to sign for all parties. This will require a little bit of lead time as well so let everyone involved know as soon as possible. The POA will have to be approved by the title company prior to the day of closing.

Let’s Prepare for Closing Day!

As we get close to day of closing here is a quick checklist:

Set up and transfer utilities (sometimes water makes you wait until day of closing.)

Review the ALTA with your agent

Call the title company to discuss wiring instructions if money is due for closing. *Do NOT trust any email! Always call to verify instructions!*

Double check dates and times with your movers - you cannot access the property until everythin with movers you cannot access the property until closing is final!

What Happens After Closing?

Congratulations! Day of Closing belongs to YOU! You‘ll walk out of closing and get to enjoy your home right away! Next steps:

Change your locks

Forward your mail

Get to know your new HOA (if you have one)

Make sure to know what is covered by your home warranty (if you have one)

Now you can order the furniture and/or appliances you‘ve been eyeing!

What Now?

If you’ve made it this far, you’re definitely serious about your home search. Please reach out to me to get the process started

– I’m looking forward to working with you!

Florida Association of REALTORS As-Is Contract

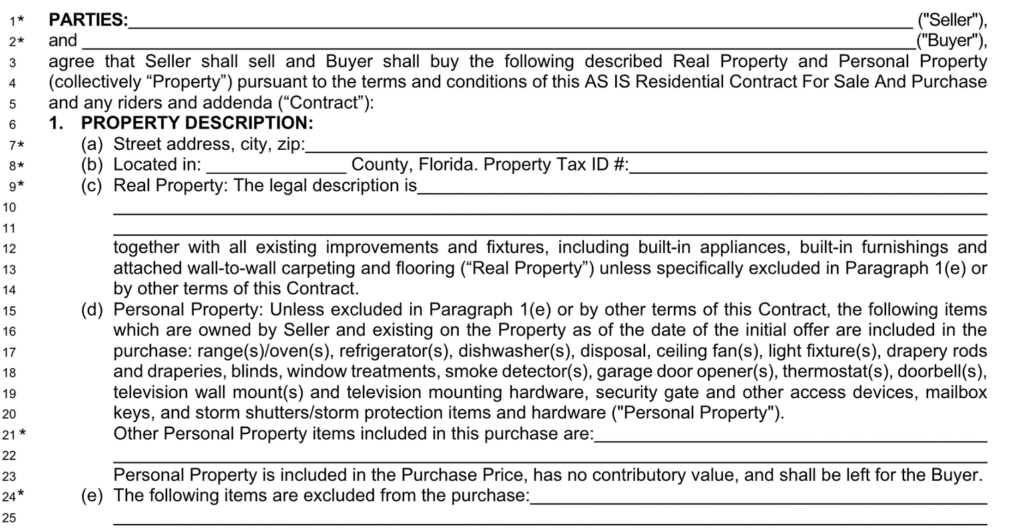

This section describes the “parties” (the buyer and seller), as well as a legal description of the property being bought/sold.

It also defines what personal property is included or excluded from the sale. You want that washer and dryer? What about the swing in the back yard? Make sure it’s listed here!

This section describes the “parties” (the buyer and seller), as well as a legal description of the property being bought/sold.

Florida Association of REALTORS As-Is Contract

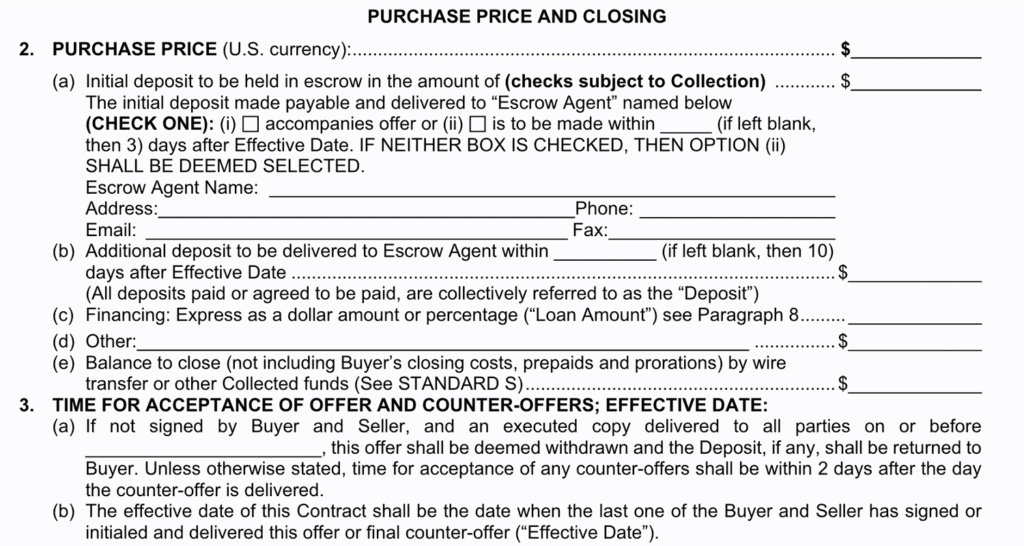

Section 2 is where the money details are listed. The purchase price, the earnest money deposit, financing, and the final balance due.

Section 3 provides the deadline for an acceptance of the buyer’s offer and defines the effective date (when both parties have signed and the contract has been delivered).

Section 2 is where the money details are listed. The purchase price, the earnest money deposit, financing, and the final balance due.

Section 3 provides the deadline for an acceptance of the buyer’s offer and defines the effective date (when both parties have signed and the contract has been delivered).

Florida Association of REALTORS As-Is Contract

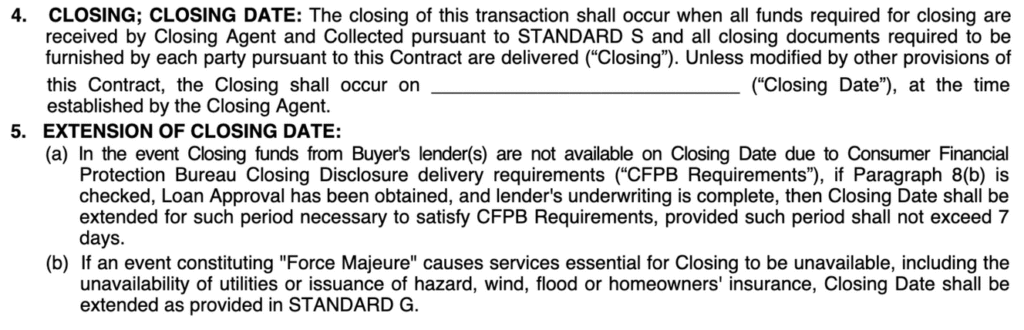

Section 4 provides the closing date. It may say “on or before.”

Section 5 provides options for extending the closing date when necessary. For example, if the lender needs more time to provide funds for closing.

Section 4 provides the closing date. It may say “on or before.”

Section 5 provides options for extending the closing date when necessary. For example, if the lender needs more time to provide funds for closing.

Florida Association of REALTORS As-Is Contract

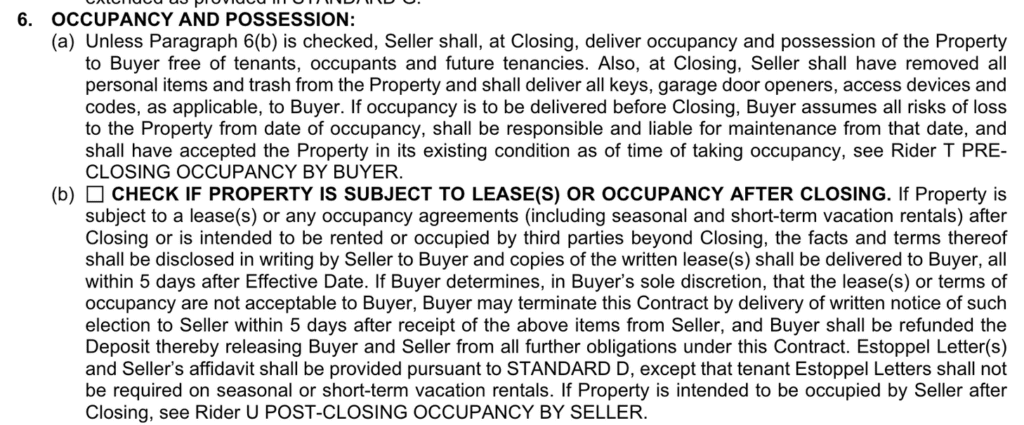

Section 6 details when the seller no longer occupies the property, and when the buyer is allowed to take occupancy. Day of closing belongs to the buyer. The entire day!

It also provides an area to indicate whether or not the property is subject to a lease by a tenant – short or long term. (STR needs addendum.)

Section 6 details when the seller no longer occupies the property, and when the buyer is allowed to take occupancy. Day of closing belongs to the buyer. The entire day!

It also provides an area to indicate whether or not the property is subject to a lease by a tenant – short or long term. (STR needs addendum.)

Florida Association of REALTORS As-Is Contract

Section 7 gives an option to let the buyer have the right to “assign” the contract to someone else. Assigning the contract means the buyer can give the right and responsibility to purchase the responsibility to someone else.

1: Never (Wholesale) 2: When an investment 3: When an owner/occ

Section 7 gives an option to let the buyer have the right to “assign” the contract to someone else. Assigning the contract means the buyer can give the right and responsibility to purchase the responsibility to someone else.

1: Never (Wholesale) 2: When an investment 3: When an owner/occ

Florida Association of REALTORS As-Is Contract

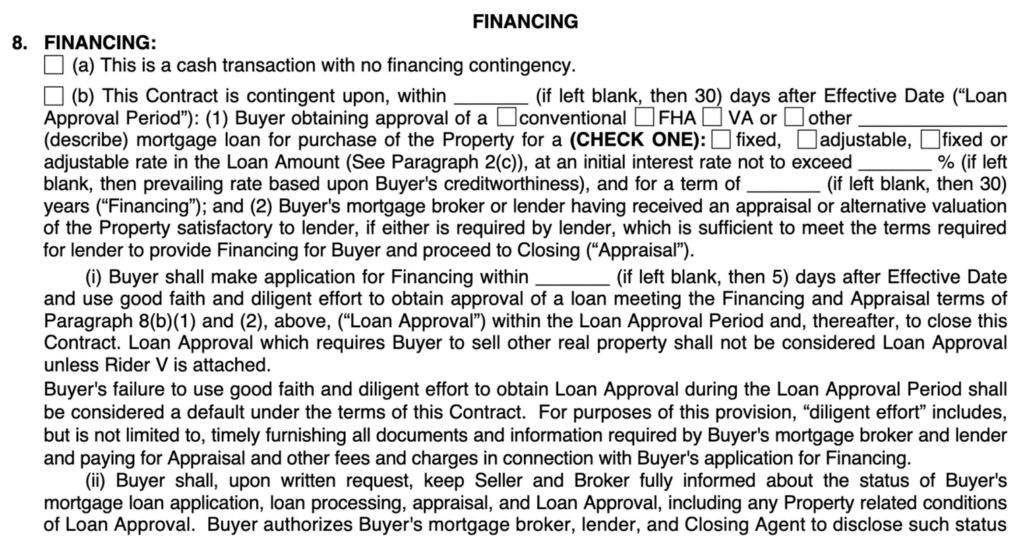

Section 8 describes the details for the financing (or lack thereof). It also describes the buyer’s responsibility and liability for obtaining financing and what happens if they don’t put in good faith effort to do so.

Regarding 8b: Financing period should be the same as contract term when possible. This includes appraisal.

Section 8 describes the details for the financing (or lack thereof). It also describes the buyer’s responsibility and liability for obtaining financing and what happens if they don’t put in good faith effort to do so.

Regarding 8b: Financing period should be the same as contract term when possible. This includes appraisal.

Florida Association of REALTORS As-Is Contract

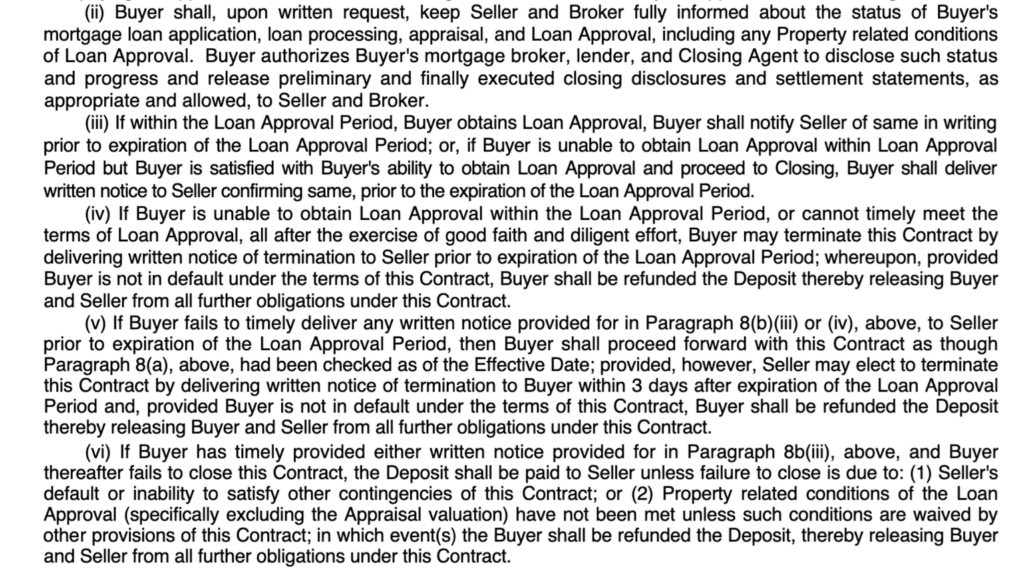

Section 8, part 2.

ii: Agents have authority to speak with the lender

iii: Loan approval notice requirements

iv: Reference Line 89 in 8b

v: If notice not given, it’s like a cash transaction now and seller can deliver notice to cancel

vi: Who gets the EMD

Section 8, part 2.

ii: Agents have authority to speak with the lender

iii: Loan approval notice requirements

iv: Reference Line 89 in 8b

v: If notice not given, it’s like a cash transaction now and seller can deliver notice to cancel

vi: Who gets the EMD

Florida Association of REALTORS As-Is Contract

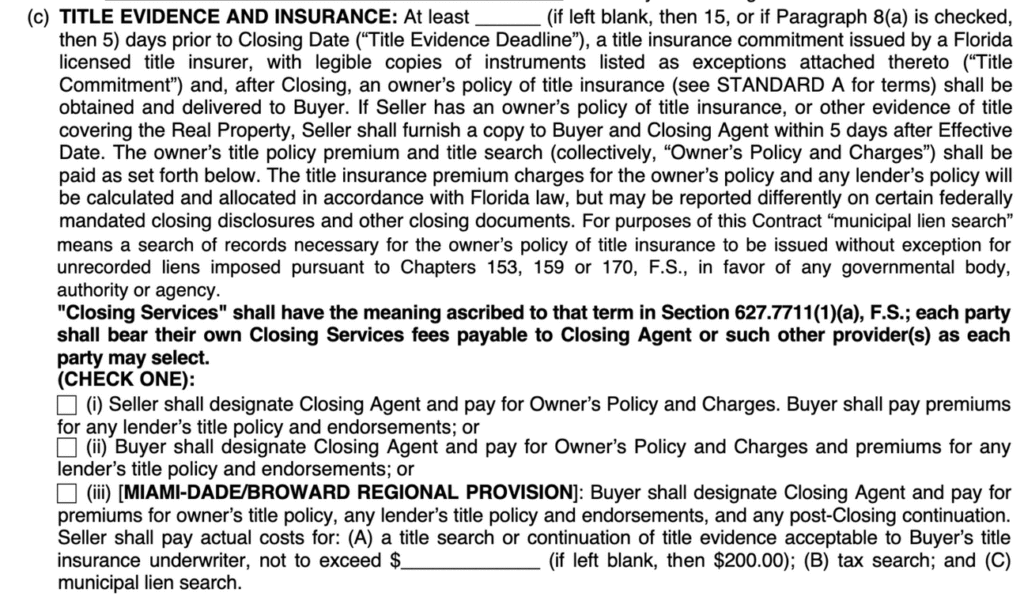

Section 9 talks about the various closing costs of the transaction, and clarifies who will pay for what.

This is also where payment and timelines for title insurance, surveys, home warranties, and special assessments are described.

Section 9 talks about the various closing costs of the transaction, and clarifies who will pay for what.

This is also where payment and timelines for title insurance, surveys, home warranties, and special assessments are described.

Florida Association of REALTORS As-Is Contract

Section 9, part 2, goes through the various closing costs of the transaction, and clarifies who will pay for what.

If you have a financed transaction, this will be left blank.

Title selection is one of the most important parts of the transaction. Build your team!

Section 9, part 2, goes through the various closing costs of the transaction, and clarifies who will pay for what.

If you have a financed transaction, this will be left blank.

Title selection is one of the most important parts of the transaction. Build your team!

Florida Association of REALTORS As-Is Contract

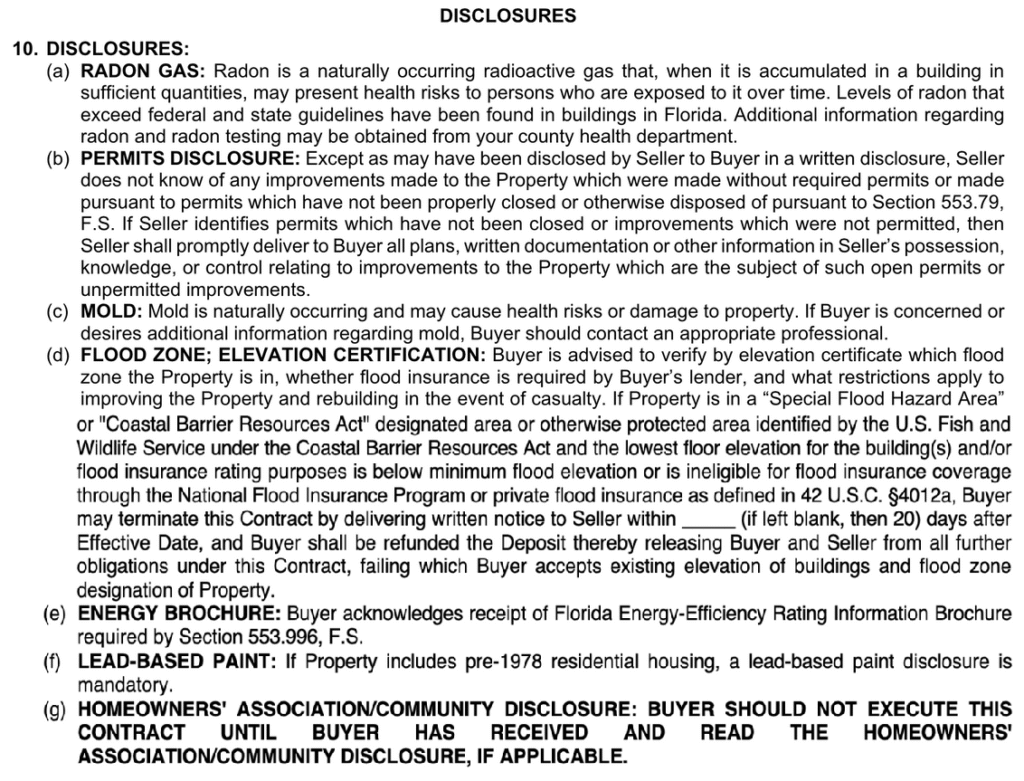

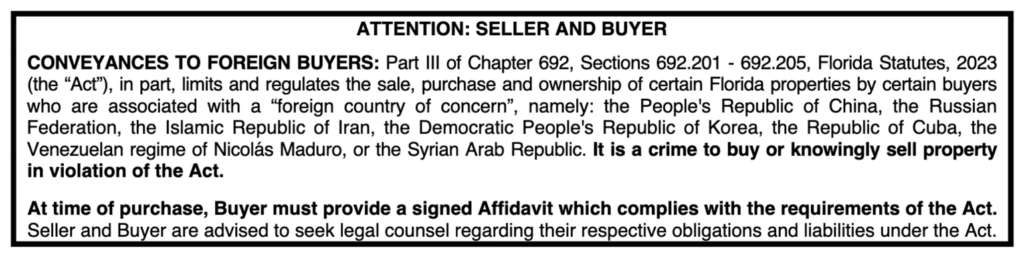

Section 10 describes all the disclosures that you, the buyer, can expect.

d: There is a new flood disclosure as well. Not referenced here but may be one day. Understand CBRA Zones.

e: We require proof of this disclosure,

f: Mandatory as well

g: Request these documents before you sign

Section 10 describes all the disclosures that you, the buyer, can expect.

d: There is a new flood disclosure as well. Not referenced here but may be one day. Understand CBRA Zones.

e: We require proof of this disclosure,

f: Mandatory as well

g: Request these documents before you sign

Florida Association of REALTORS As-Is Contract

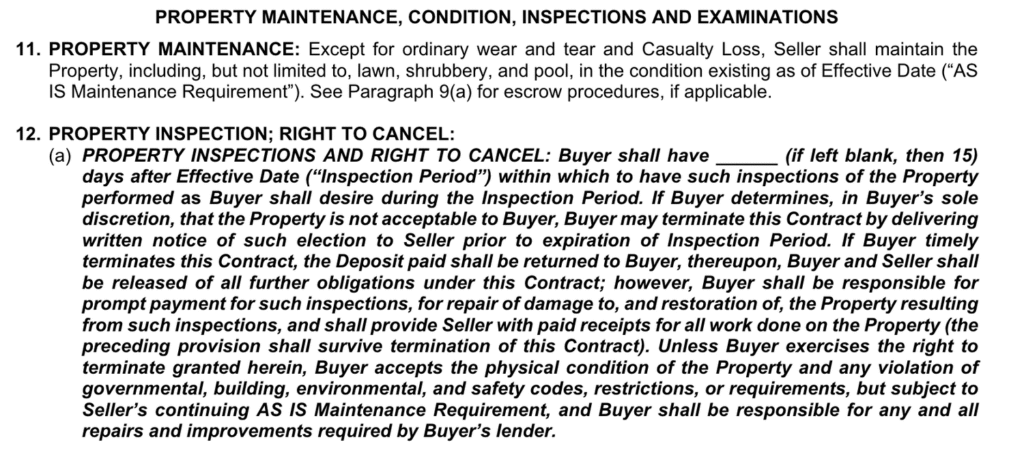

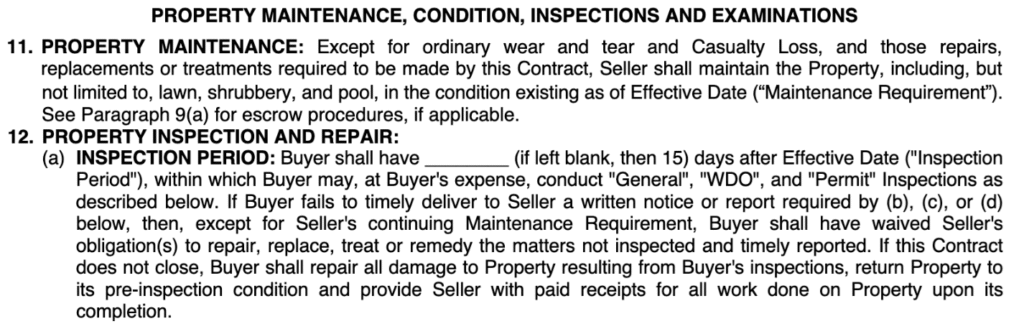

Section 11 says that the seller will maintain the property in the condition it was in at the time of an offer submission (other than ordinary wear and tear).

Section 12 gives the buyer the right to have a home inspection, and the right to cancel the contract for any reason at all. This is NOT in the standard contract but can be accomplished through As-Is Addn but is not accepted generally.

Section 11 says that the seller will maintain the property in the condition it was in at the time of an offer submission (other than ordinary wear and tear).

Section 12 gives the buyer the right to have a home inspection, and the right to cancel the contract for any reason at all. This is NOT in the standard contract but can be accomplished through As-Is Addn but is not accepted generally.

Florida Association of REALTORS As-Is Contract

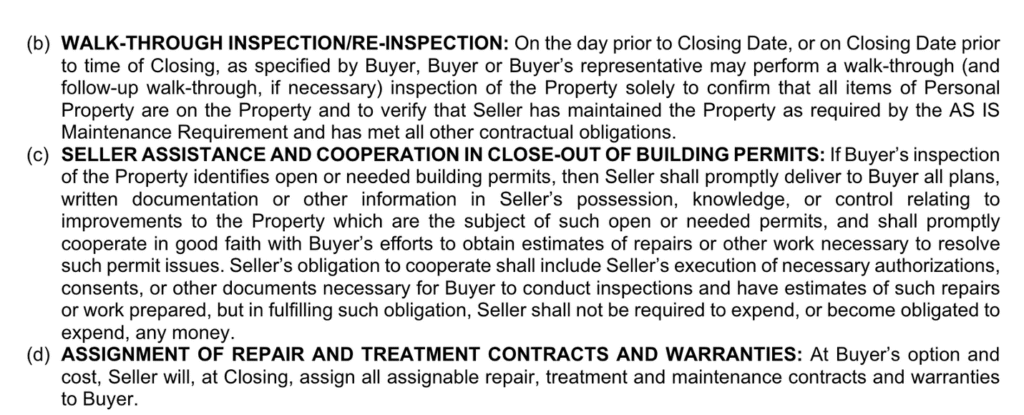

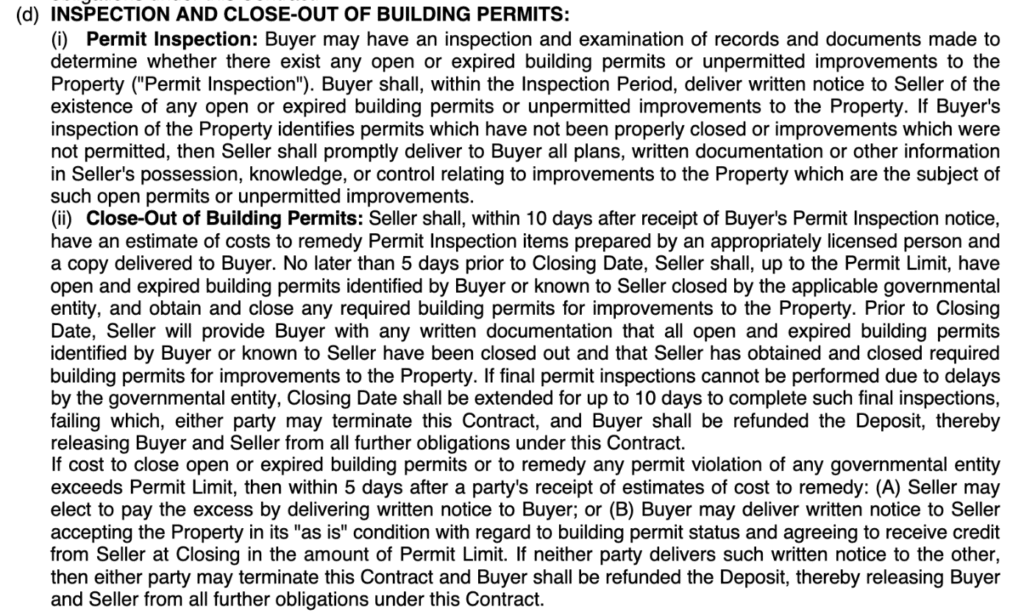

Section 12 also includes details on the buyer’s right to do a walk through inspection prior to closing, the fact that a seller will help in closing out open building permits, and that the seller will assign contracts to the buyer if desired.

Section 12 also includes details on the buyer’s right to do a walk through inspection prior to closing, the fact that a seller will help in closing out open building permits, and that the seller will assign contracts to the buyer if desired.

Florida Association of REALTORS As-Is Contract

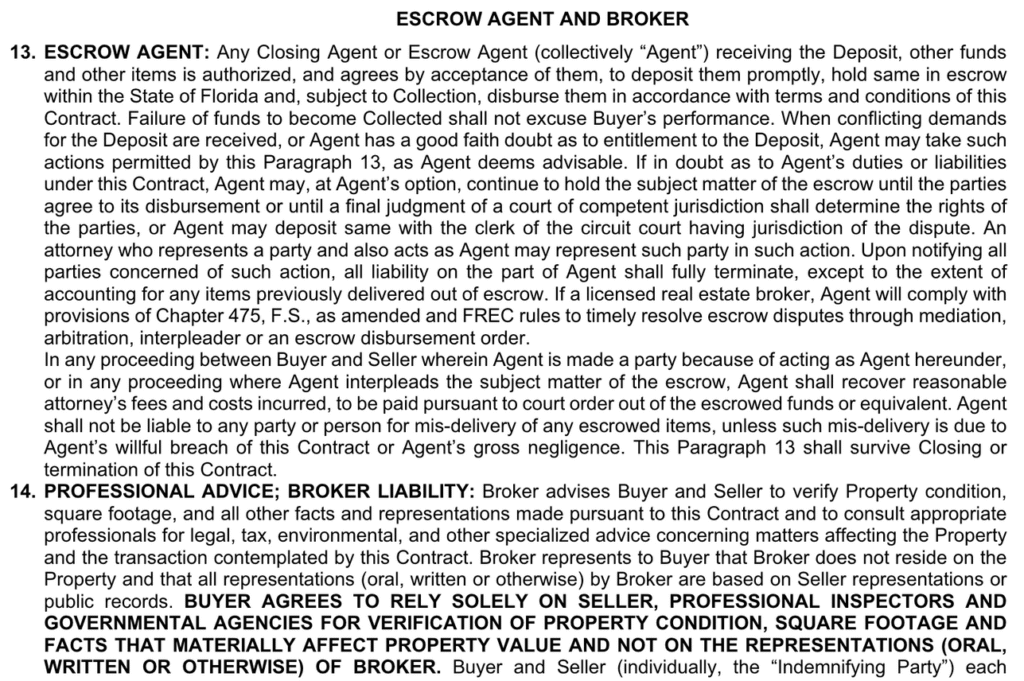

Section 13 describes the role and responsibilities of the escrow agent.

Section 14 describes the role and liability of the brokers and their agents during the transaction.

Section 13 describes the role and responsibilities of the escrow agent.

Section 14 describes the role and liability of the brokers and their agents during the transaction.

Florida Association of REALTORS As-Is Contract

Section 15 details the circumstances in which a buyer or seller will be in default on their responsibilities in the contract.

Section 16 and 17 details how any disputes and resulting attorney’s fees will be handled.

Section 15 details the circumstances in which a buyer or seller will be in default on their responsibilities in the contract.

Section 16 and 17 details how any disputes and resulting attorney’s fees will be handled.

Florida Association of REALTORS As-Is Contract

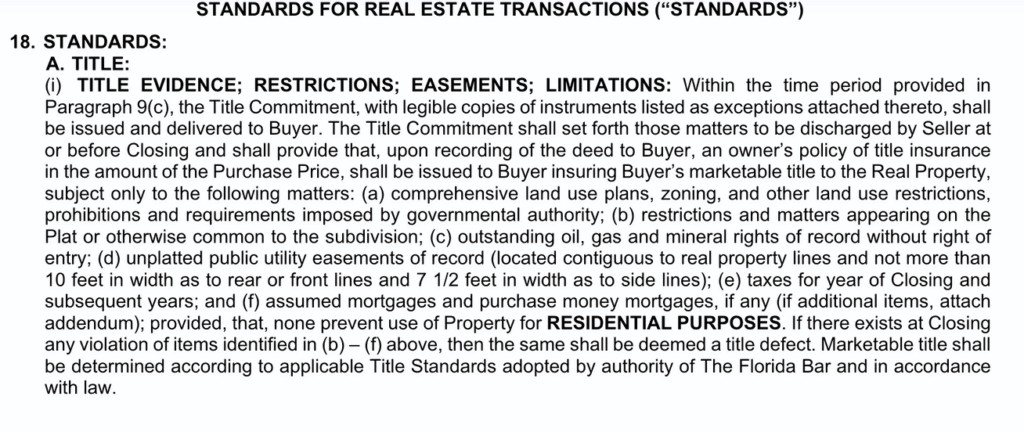

Section 18 contains definitions and sets expectations for various aspects of: title (including things like easements); surveys; leases; liens (i.e. if the seller owes someone money and the property is their collateral); timing and procedural details of the transaction and closing process; prorations of taxes or money owed; and the contract itself.

Section 18 contains definitions and sets expectations for various aspects of: title (including things like easements); surveys; leases; liens (i.e. if the seller owes someone money and the property is their collateral); timing and procedural details of the transaction and closing process; prorations of taxes or money owed; and the contract itself.

Florida Association of REALTORS As-Is Contract

Within section 18, standard X is worth calling out. This paragraph describes the buyer’s waiver of any claims against the Seller regarding the physical condition of the property at the time of closing. This is where the buyer is accepting the property “as is” – and it’s why section 10 is so important. If the buyer doesn’t accept the property’s condition, they should cancel within the inspection period.

Florida Association of REALTORS As-Is Contract

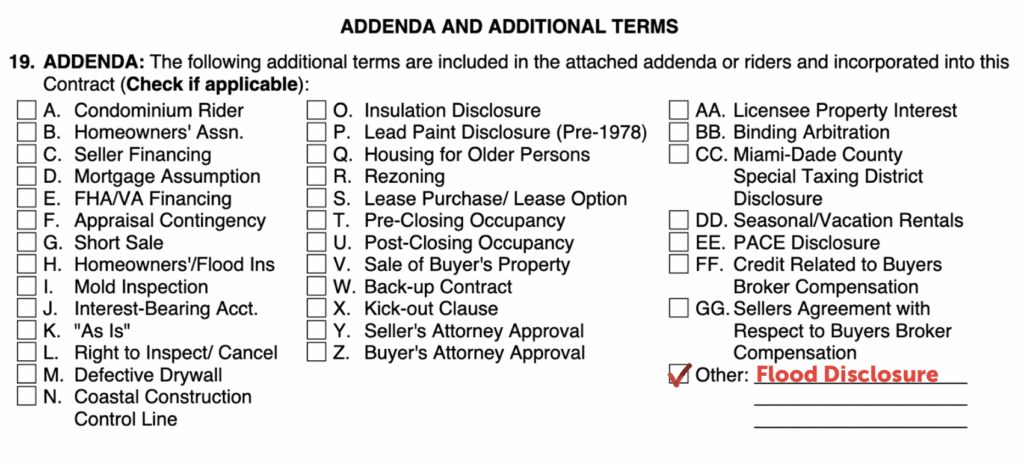

Section 19 is a checklist of all the additional contractual items that may be necessary. If you see items checked here, there will be accompanying documents to sign.

**IF YOU ARE OFFERING ON A CONDO BOX A WILL BE MARKED AS WELL**

Section 19 is a checklist of all the additional contractual items that may be necessary. If you see items checked here, there will be accompanying documents to sign.

**IF YOU ARE OFFERING ON A CONDO BOX A WILL BE MARKED AS WELL**

Florida Association of REALTORS As-Is Contract

Section 9 outlines buyer side closing costs but most importantly, it covers the prenegotiated amount of money “left on the table” in the event remedies are needed.

Section 9 outlines buyer side closing costs but most importantly, it covers the prenegotiated amount of money “left on the table” in the event remedies are needed.

Florida Association of REALTORS As-Is Contract

Sections 11 and 12 cover the property maintenance and condition expectations. It also outlines the buyers inspection period requirements.

Sections 11 and 12 cover the property maintenance and condition expectations. It also outlines the buyers inspection period requirements.

Florida Association of REALTORS As-Is Contract

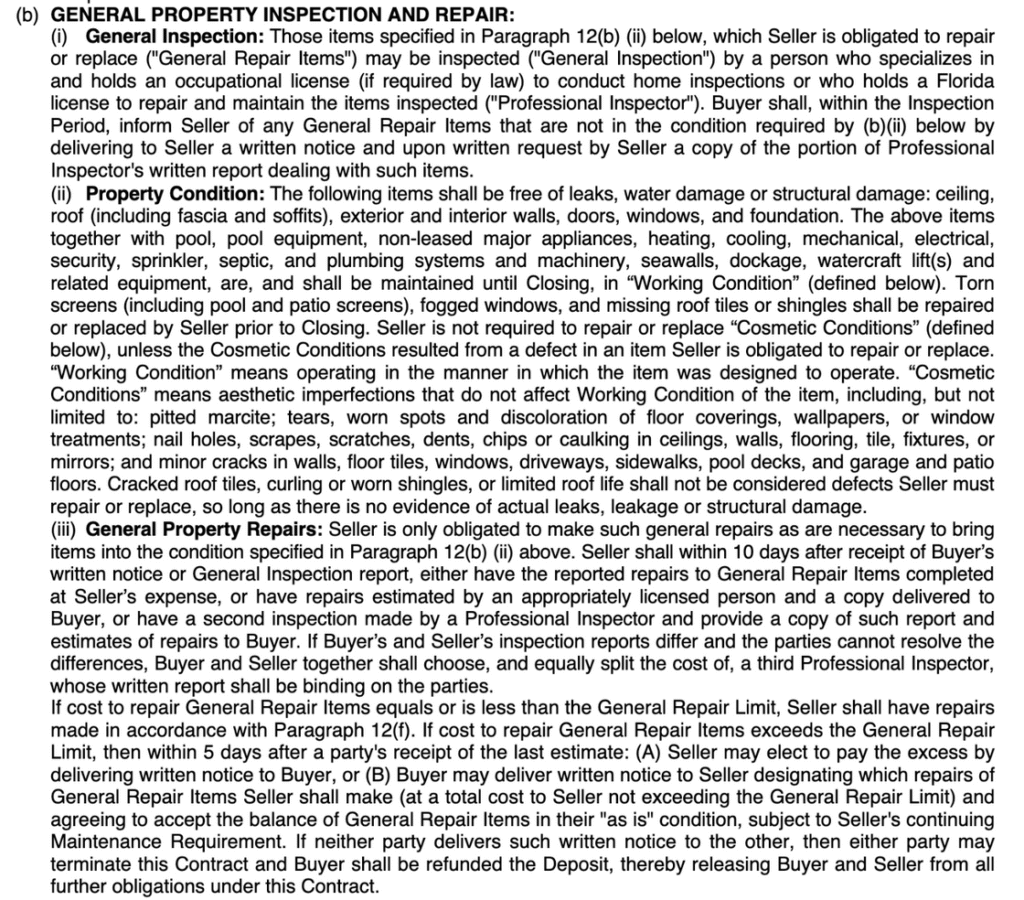

This section covers what the seller is and is not responsible to repair or replace as a part of your inspections.

What is considered cosmetic is outlined here.

This section covers what the seller is and is not responsible to repair or replace as a part of your inspections.

What is considered cosmetic is outlined here.

Florida Association of REALTORS As-Is Contract

12 C details WDO inspection and repair protocol.

12 C details WDO inspection and repair protocol.

Florida Association of REALTORS As-Is Contract

12 D details closing out building permits.

12 D details closing out building permits.

Florida Association of REALTORS As-Is Contract

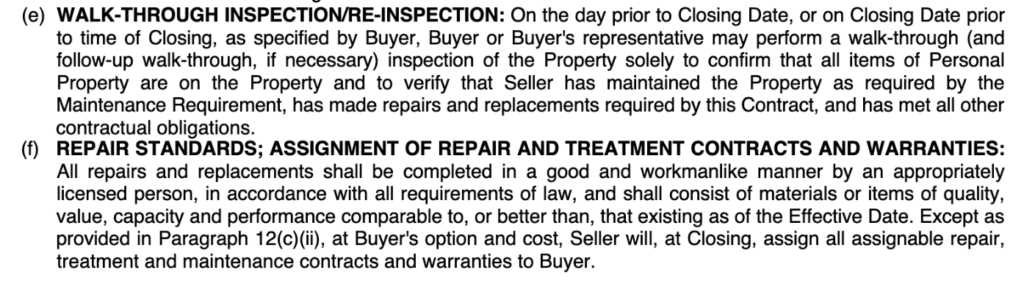

12 E & F covers walk through access and repair standards.

12 E & F covers walk through access and repair standards.

The final statement of all parties’ financial requirements will be expressed on the ALTA if you’re using a loan product. If you have a cash buyer, you will work from a HUD-1.

There should be no surprises on this statement.

The ALTA can range from 1 to 3 pages in length and while it has been reviewed by the title company, lender, then you will receive it. Please do not ONLY check your commissions.

Take the time to review all lines and really understand this document. It’s the culmination and interpretation of the contract agreements.

Final Settlement

Statement,

aka the ALTA

The final statement of all parties’ financial requirements will be expressed on the ALTA if you’re using a loan product. If you have a cash buyer, you will work from a HUD-1.

There should be no surprises on this statement.

The ALTA can range from 1 to 3 pages in length and while it has been reviewed by the title company, lender, then you will receive it. Please do not ONLY check your commissions.

Take the time to review all lines and really understand this document. It’s the culmination and interpretation of the contract agreements.

Final Settlement Statement, aka the ALTA

On this page, you can see real estate commissions, title charges, HOA dues, recording fees, state taxes, and any bills that need to be paid as a part of settling the contract.

Final Settlement Statement, aka the ALTA

On this page, you can see real estate commissions, title charges, HOA dues, recording fees, state taxes, and any bills that need to be paid as a part of settling the contract.

Licensed Realtor, FL License #SL3560845

Specializing in vacation homes and investment properties

Based in Destin and serving a 60‑mile radius from Fort Walton Beach to 30A